A 2025 study found that the State of Housing in Black America (SHIBA) delivers a sobering assessment of the housing landscape for Black households. Despite modest macroeconomic improvements, systemic barriers continue to suppress Black homeownership, wealth building, and access to equitable mortgage financing.

More than 57 years after the Fair Housing Act, the Black + White and non-white homeownership gap remains above 30 percentage points. A stark reminder that housing inequality remains one of America’s most persistent economic challenges.

1. Mortgage Credit Remains Tight and Harder for Black Borrowers

Mortgage credit conditions in 2024 remained restrictive. The Mortgage Bankers Association’s credit availability index closed 2024 at 96.6, far below its 2019 peak of 189.8. Lending standards tightened considerably:

-

Median FICO score at origination increased from 741 (2019) to 748 (2024)

-

First-time buyers needed a median score of 724 in 2024, up from 712 in 2019

Structural Barriers Behind Credit Gaps: The disparities go beyond credit scores:

-

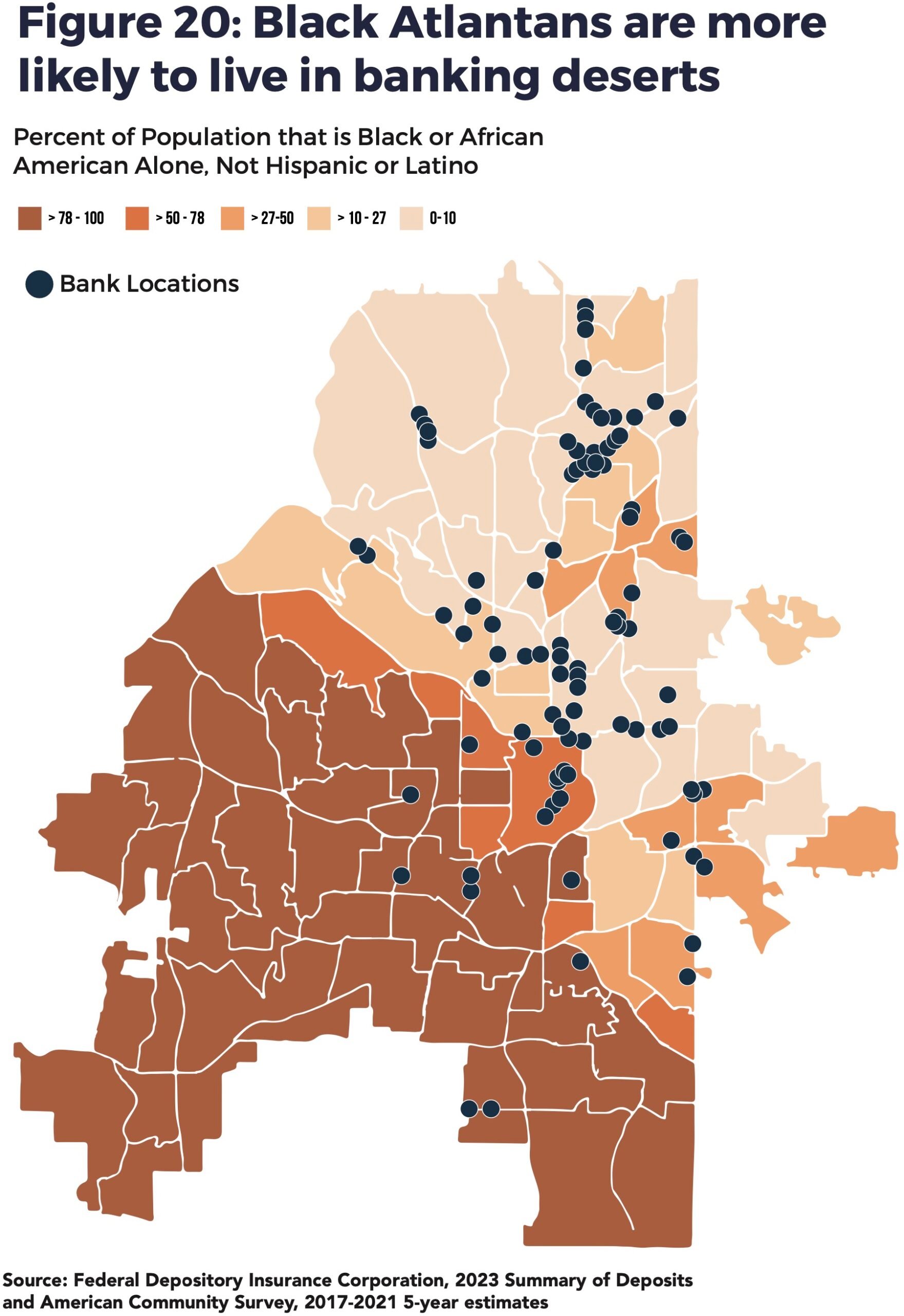

13% of Black households are unbanked, compared to 3% of White households.

-

Majority-Black neighborhoods lost 6.6% of bank branches between 2020 and 2023

-

14% of Black consumers are credit invisible, compared to 9% of Whites

These “bank deserts” push families toward high-cost alternative lending that doesn’t build credit history, reinforcing a cycle of exclusion and wealth-building insolvency.

2. Automated Underwriting Still Produces Unequal Outcomes

Automated underwriting systems (AUS), designed to reduce bias, still generate unequal results.

-

70% of Black applications assessed through AUS were approved

-

Compared to 81% for White applicants

Even as agencies begin incorporating rental payment history and cash-flow data, adoption has been limited, with only about 6,000 applications having been accepted based on rental history as of August 2024.

The report argues that reliance on traditional financial metrics (debt-to-income ratios, credit history, and loan-to-value) continues to reflect deeper wealth inequality rather than true borrower risk.

3. Black Millennial Buyers Face Different Market Realities

The report highlights sharp differences between Black and White millennial borrowers:

-

43% of White millennial borrowers earned above 120% of Area Median Income (AMI), compared to only 27% of Black millennial borrowers

-

71% of White millennials secured conventional loans versus 38% of Black millennials

-

56% of Black millennial buyers purchased in majority-minority neighborhoods compared to just 13% of White buyers

This suggests Black millennials are:

-

More likely to rely on FHA or non-conventional financing

-

More concentrated in lower-income or segregated neighborhoods

-

Building wealth in markets where appreciation and capital access may lag

4. Appraisal Bias Continues to Suppress Black Wealth

One of the report’s most powerful sections examines valuation bias. NAREB’s expanded appraisal research found that in majority-Black neighborhoods where Black borrowers were actively originating mortgages, homes were appraised at significantly lower values.

Prior research cited in the report shows:

-

Homes in predominantly Black neighborhoods are undervalued by 21–23%

-

Resulting in an estimated $156 billion in lost Black household wealth

Freddie Mac also found that appraisals fall below contract value more than twice as often in minority neighborhoods. The report warns that, if not reformed, automated valuation models (AVMs) could amplify these biases digitally.

5. Policy Recommendations: A Civil Rights Approach to Housing

-

Limit speculative investor activity in starter-home markets

-

Modernize lending standards to promote fair access

-

Strengthen appraisal oversight and standardize fair-valuation frameworks

-

Increase transparency in automated valuation models

-

Stabilize homeowners' insurance markets

The report emphasizes that homeownership is not just an economic goal but also a civil rights imperative.

Housing Equity Is Wealth Equity

Black homeownership remains the foundation of Black wealth, but the system still produces unequal outcomes at nearly every stage of the mortgage process.

From tighter credit standards to valuation bias, from banking access to investor activity, the barriers are structural, not individual.

The path forward requires:

-

Modernized underwriting

-

Fair valuation reform

-

Investor regulation

-

Expanded down payment support

-

Accountability across federal housing policy

Until those changes are implemented at scale, the racial homeownership gap will remain one of America’s most persistent wealth divides.